The belief that people are loyal to brands is coming under increasing fire. I have been privileged to witness and contribute to brand loyalty’s fascinating evolution. Now a new study and article in Harvard Business Review from Christof Binder and Dominique M. Hanssens, Why Strong Customer Relationships Trump Powerful Brands, gives the topic fresh context and sets up intriguing questions as to where branding’s value and investment is heading.

Historically, branding has been deployed with the same intent as advertising. That is, create awareness, prompt trial, and encourage adoption. For the last twenty years or so branding has largely been used as Tom Peters identified, “as a sorting device.” The overriding goal of branding in this period was to make a company, product or service stand out. “Top-of-mind” was thought to lead to a disproportionate “share of wallet”.

Loyalty has always been inferred in branding. If one was delivering a brand that matched the value, beliefs and practices of certain consumers it was believed those people would be loyal to the brand. This gave way to the term ‘brand evangelists’ which has been overused and never properly defined (or delineated from word-of-mouth). Through this period, practitioners like myself largely subscribed to Philip Kotler’s four types of loyal consumers:

- Hard-core Loyals: those who buy the same brand consistently

- Split Loyals: those loyal to two or three brands

- Shifting Loyals: those who move from one brand to another

- Switchers: those with no loyalty

There has been great debate on the erosion of brand loyalty. It has already produced a new  term that I find entertaining, “consumer promiscuity”. At first, this promiscuity was driven by consumers interested in finding a better price or deal elsewhere. Now this brand philandering takes place any time consumers believe their complex wants and needs are not being met. This relates to another new marketing term (we marketers love to name things) and that is, “chameleon consumers”. These consumers defy traditional segmentation (on a side note…most marketers today are terrible at segmentation). Chameleons are hard to read and hard to please making it difficult for brands to hold onto them.

term that I find entertaining, “consumer promiscuity”. At first, this promiscuity was driven by consumers interested in finding a better price or deal elsewhere. Now this brand philandering takes place any time consumers believe their complex wants and needs are not being met. This relates to another new marketing term (we marketers love to name things) and that is, “chameleon consumers”. These consumers defy traditional segmentation (on a side note…most marketers today are terrible at segmentation). Chameleons are hard to read and hard to please making it difficult for brands to hold onto them.

This supports findings from Nielsen and EY who have reported on the decline in trust of advertising and decreasing loyalty to brands. These findings have concerned businesses but instead of addressing it and taking advantage of the situation they continue to invest traditionally in branding and marketing. This leads us to the current study.

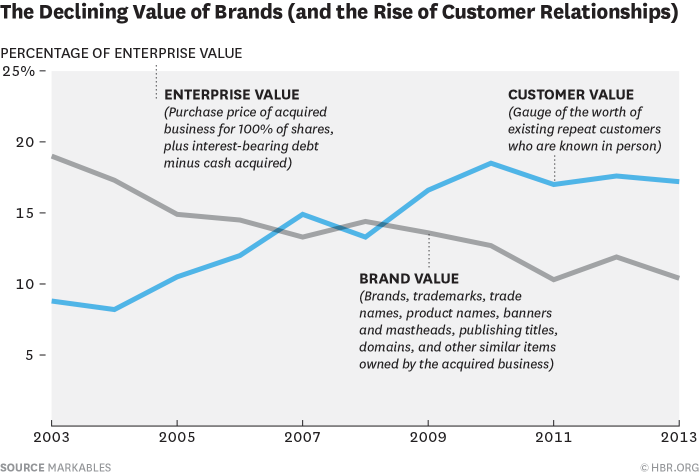

The authors “looked at the value of brands and customer relationships as revealed by M&A data covering over 6,000 mergers and acquisitions worldwide between 2003 and 2013.” As they say, “The beauty of M&A for examining valuation trends is that M&As reveal the dollar valuations of all assets at the time of the acquisition. Upon acquiring a business, companies have to value the different assets they acquired for their accounts and balance sheet in accordance with accounting and reporting standards.”

This points to the authors’ bold conclusion, “These numbers reveal a dramatic shift in the strategic approach to marketing over the last 10 years. Acquirers have decisively moved from investing into businesses with strong brands to businesses with strong customer relationships.” The graph shows that brand valuations declined by nearly half while customer relationship values doubled over the decade.

Part of this shift is attributed to digital marketing that allows for more accurate personalization of messaging and is more cost effective than traditional brand management. The latter is now far too expensive or limited in potential because of the maturity of markets and industries. What it really means is ubiquity is no longer the goal. Broad brand awareness does not guarantee value so “M&A strategies now concentrate more on acquiring firms with strong customer relationships – with all the loyalty and cross-selling benefits that confers.”

Binder and Hanssens point out that “purchasing decisions have become more fact based, and less brand-image based.” Then they hedge just a bit, “Customers still value strong brands, but what constitutes a strong brand is now more dependent on customers’ direct experience with an offering, and with their relationship with the firm that produces it.”

The real lesson is…branding has not adequately moved beyond awareness and engagement. It is stuck in its own past. Branding is the most strategic tool in the arsenal to ensure loyalty but is being poorly applied or not applied to this valuable task. I have been in this business a long time and agree that loyalty has been a glaring missing ingredient of branding. This has to be at forefront of the brand agenda for both companies and brand consultancies.

Finally, the authors suggest this is “a reality check on some of the gigantic brand values now published by leading brand valuation companies as it reveals that often the lion’s share of value lies in customer relationships. Although closely intertwined, brand equity and customer equity are different concepts that need to be measured and reported separately.” I am pleased they call this out because there are too many brand rankings and brand value methodologies these days. Their numbers strain credibility and the underlying assumptions are questionable.

published by leading brand valuation companies as it reveals that often the lion’s share of value lies in customer relationships. Although closely intertwined, brand equity and customer equity are different concepts that need to be measured and reported separately.” I am pleased they call this out because there are too many brand rankings and brand value methodologies these days. Their numbers strain credibility and the underlying assumptions are questionable.

This study is a fantastic contribution to the practice of branding and it confirms that traditional “brand building will only go so far” in the attraction and retention of a customer. Companies ignore this at their peril.